There are many options to address progressive tax rates

It’s difficult to pass a week without seeing another attack on the Old Age Security (OAS) pension in the media. Attention is often drawn to the fact that taxpayers with incomes over $150,000 still receive at least a partial amount.

The culprit most often identified is the so-called clawback, an income tax provision that taxes OAS at a 15 per cent rate, starting at a taxable income above $90,000 in 2026. The remedy most often given is lowering the starting income well below the current threshold.

Ostensibly, the goal is to take OAS away from those rich enough that they really don’t need this income. But another way of framing this is that tax rates on better off seniors should be increased because they don’t need all their disposable income.

The implicit goal of increasing the progressivity of Canada’s tax and transfer system is laudable. But the trouble is the specific diagnosis and remedy. To assert that the fault lies entirely with the clawback is myopic and piecemeal.

The first problem is that the government doesn’t even have clear objectives for the OAS, as highlighted in a recent report of Canada’s Auditor General. Historically, the OAS has served both as an anti-poverty measure, in combination with the Guaranteed Income Supplement (GIS), and to maintain continuity of income after retirement from working, in combination with the Canadian and Quebec Pension Plan (C/QPP).

Regardless, there are numerous ways to increase the progressivity of the tax and transfer system, including specifically for the 65+ population.

The most obvious is to increase income tax rates, say for incomes above $75,000. Others could involve cutting the age deduction, removing pension income splitting or tightening the limits for Tax Free Savings Accounts (TFSAs).

But as soon as we start thinking about such alternatives, we enter the thicket of complexity. Canada’s tax and transfer system is encrusted with decades of piecemeal policy initiatives. Cavalierly touching just one part risks serious unintended consequences.

So it is with the OAS clawback.

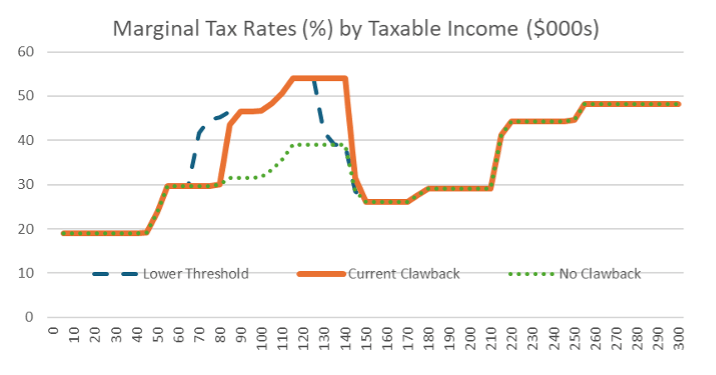

The effective marginal income tax rates for an individual in Ontario tell the story. The 15 per cent clawback starts at $90,000 and is stacked on top of federal and Ontario income tax rates. The result: an individual with $100,000 income faces a higher tax rate than anyone with income over $200,000 (54 per cent compared to 48 per cent).

The simplistic suggestion of lowering the income where the clawback starts would be worse – middle- and upper-middle income individuals would start facing unusually high tax rates.

Most people may not know which tax bracket they’re in. But they probably do know that their RRSP savings, when they start drawing them down through their RRIFs, will face a stiff rate of tax. So too would any income they’ve earned by continuing to work after age 65, an increasing trend. And of course, their investment income would also face these higher tax rates.

Canada’s tax system has been paying out money for almost half a century. Cash transfers, paid out through progams like OAS, can be seen as negative taxes; alternatively, refundable income tax credits can be seen as spending programs.

Indeed, Canada’s Tax Expenditure Account, published by the Department of Finance, shows the budgetary costs of dozens of tax provisions as if they were actual spending programs.

Focusing on OAS, and more narrowly on the clawback, is a failure to understand the full nature of Canada’s tax and transfer system. What really matters is the net effects on individuals’ disposable incomes – the impacts of all cash transfers and taxes together, given their earnings and investment incomes.

What also matters is the joint impacts of cash transfers and income taxes on an extra dollar of income – individuals’ marginal tax rates, as these can have major effects on incentives, whether to work after the usual retirement age, and how best to save for retirement in the future.

The simplistic remedy of reducing the starting income of the OAS clawback could have the unintended consequence of seriously affecting these incentives.

Beyond this, however, lies the thicket of tax and transfer complexity – not an area one enters lightly. To increase the progressivity of the tax and transfer system for older Canadians, as pushed naively by recent attacks on OAS, requires a much smarter approach, with expertise, data and simulation models.

The federal government must take a holistic approach to significant tax changes that involve Canada’s seniors – unfortunately a rarity in Canadian public policy.

Governments so far have not shown themselves up to this task.

Some sort of ongoing Observatory, possibly building on the recently created non-partisan Canadian Tax Observatory, is a promising path forward for Canada.

Photo courtesy of DepositPhotos